Insurance Formulary Tiers Explained: Tier 1, Tier 2, Tier 3, and Non-Formulary Drugs

Dec, 26 2025

Dec, 26 2025

When you pick up a prescription, you expect to pay a set amount - maybe $10, maybe $40. But what if that same drug costs $120 next month? Or worse - your plan doesn’t cover it at all? That’s where insurance formulary tiers come in. They’re the hidden system that decides how much you pay for your meds, and most people don’t understand them until they’re hit with a surprise bill.

What Exactly Is a Formulary Tier?

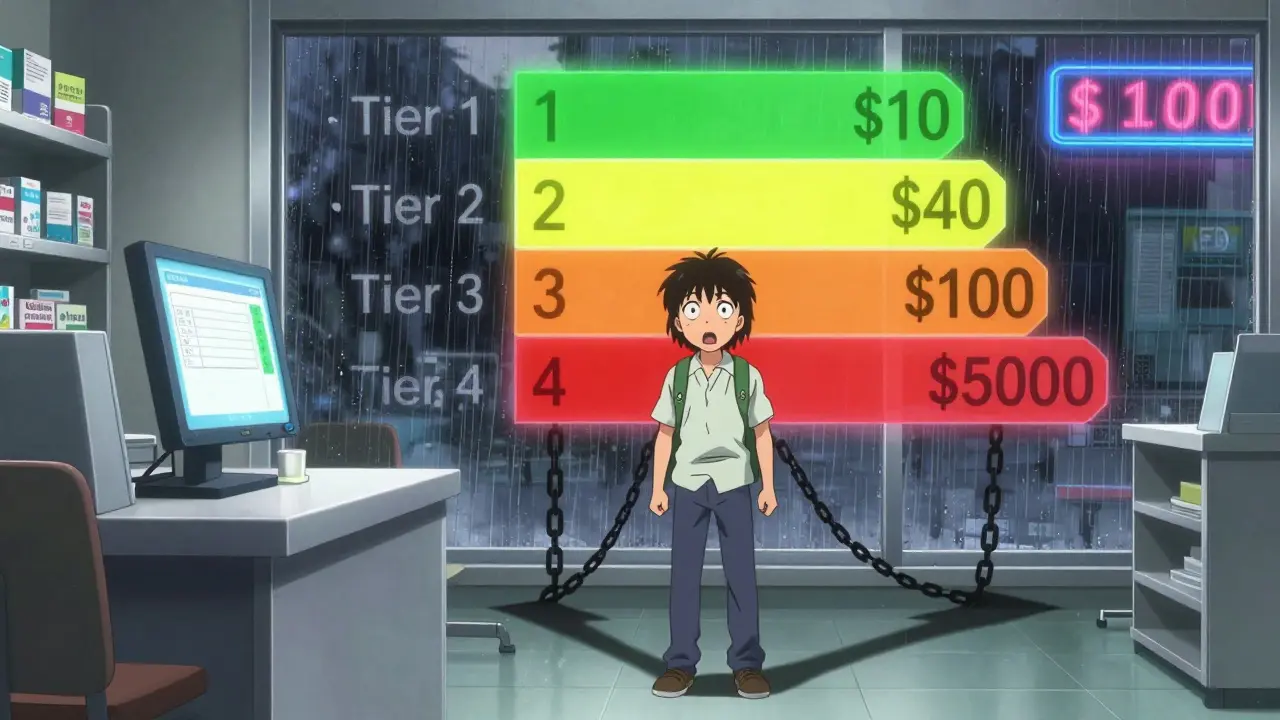

A formulary is just a list of drugs your insurance plan covers. But it’s not a simple yes-or-no list. It’s split into tiers - like levels in a video game - each with a different price tag. The higher the tier, the more you pay out of pocket. This system was created by insurance companies and Pharmacy Benefit Managers (PBMs) to push patients toward cheaper drugs while still giving access to more expensive ones when needed.Tier 1 is your cheapest option. It’s mostly generic drugs - the same medicine as the brand name, but without the fancy packaging or marketing. Think metformin for diabetes, lisinopril for high blood pressure, or atorvastatin for cholesterol. These drugs have been around for years, their patents expired, and multiple companies make them. Because of that competition, prices are low. In most plans, you pay $0 to $15 for a 30-day supply.

Tier 2 is where you find preferred brand-name drugs. These are newer or more expensive medications that your insurer has negotiated a better price on. Maybe the drugmaker gave the insurer a big discount or rebate. Examples might include brand-name versions of antidepressants like sertraline or blood pressure meds like losartan. Copays here usually run $20 to $40.

Tier 3 is the most common place for non-preferred brand-name drugs. These are drugs with no generic available, or where the insurer didn’t get a good deal on them. They’re still covered, but you pay more - often $50 to $100 per prescription. Drugs like Humira for rheumatoid arthritis or Ozempic for diabetes often land here. If your doctor prescribes one of these, you’ll feel the pinch unless you qualify for an exception.

Some plans go even further. Tier 4 and Tier 5 exist for specialty drugs - things like cancer treatments, rare disease meds, or injectables that cost hundreds or thousands per month. These aren’t paid with a flat copay. Instead, you pay a percentage - 25% to 50% - of the total drug cost. That means a $10,000 drug could cost you $5,000 before insurance kicks in. These tiers are where most people get stuck, and where the system breaks down.

What Does ‘Non-Formulary’ Mean?

Non-formulary drugs aren’t on your plan’s list at all. That doesn’t mean they’re unsafe or ineffective. It just means your insurer decided not to cover them - usually because they’re too expensive, there’s a cheaper alternative, or they don’t meet clinical guidelines. You might find your favorite migraine med or a specific thyroid drug in this category.If your doctor prescribes a non-formulary drug, you have two choices: pay full price (which could be $300 or more), or ask for a formulary exception. This is a formal request, usually started by your doctor, asking the insurer to cover the drug anyway. You’ll need to prove medical necessity - like if you tried all the Tier 1 and Tier 2 options and they didn’t work, or if you have an allergy to them. Approval can take days or weeks. In the meantime, you might have to go without your medication.

One real-world example: a patient in Edinburgh was prescribed a specific antipsychotic for schizophrenia. It wasn’t on their plan’s formulary. Their doctor submitted an exception, included lab results and past treatment failures, and got it approved after 11 days. Without that process, they’d have paid £450 a month out of pocket.

Why Do Tiers Change - And Why Does It Matter?

Formularies aren’t set in stone. They can change quarterly. A drug you’ve been taking for years might suddenly jump from Tier 2 to Tier 3 - no warning, no explanation. This happens because PBMs renegotiate deals with drugmakers. If a company stops offering rebates, the insurer moves the drug to a higher tier to save money.That’s why you can’t just assume your meds will stay cheap. A 2022 survey found that 43% of people on commercial plans had at least one drug moved to a higher tier during the year. For seniors on Medicare Part D, the same thing happens. You might get a notice in the mail - or you might not. Many people only find out when they go to the pharmacy and the price is double what they expected.

This unpredictability is one of the biggest complaints. A 2023 study showed 61% of patients couldn’t accurately guess how much their prescription would cost before filling it. That’s not just inconvenient - it’s dangerous. People skip doses or stop taking meds altogether because they can’t afford the surprise cost.

How to Find Out What Tier Your Drug Is On

You don’t have to guess. Every insurance plan must give you access to its full formulary list - usually online or by phone. Here’s how to do it:- Log into your insurer’s member portal. Look for “Drug Formulary,” “Prescription Benefits,” or “Medication List.”

- Search for your drug by name. Make sure to try both brand and generic versions.

- Check the tier. Note whether it’s a copay or coinsurance.

- Look for any restrictions - like prior authorization or step therapy (you have to try cheaper drugs first).

- Print or save the page. Keep it with your medical records.

Medicare beneficiaries can use the Medicare Plan Finder tool to compare formularies across Part D plans. Commercial plan users should check their Summary of Benefits and Coverage (SBC) document - it has a simplified version of the formulary.

Third-party tools like GoodRx or SingleCare can help too. They show you cash prices and sometimes even list what tier a drug is on for major insurers. But don’t rely on them alone - your plan’s official list is the only one that matters.

What to Do If Your Drug Is in a High Tier or Non-Formulary

If your medication is expensive or not covered, you’re not stuck. Here’s what works:- Ask your doctor for alternatives. Is there a generic? A Tier 1 or 2 drug that works just as well? Sometimes switching from a brand-name statin to a generic version saves $200 a month.

- Request a formulary exception. Your doctor fills out a form explaining why you need this drug. Include medical records, past treatment failures, or side effects from other options. Many approvals happen within a week.

- Use a patient assistance program. Drugmakers like AbbVie, Novo Nordisk, and Pfizer have programs that give free or low-cost meds to people who qualify based on income.

- Check for coupons or discounts. GoodRx, RxSaver, and even the drugmaker’s own website may offer savings cards that cut the price in half.

- Consider switching plans during open enrollment. If you’re on Medicare or an employer plan, you can switch to a different plan next year that covers your meds better. Look at the formulary before you enroll.

One patient in Glasgow had a rare autoimmune disease. Her drug was Tier 5 - 40% coinsurance. She paid £800 a month. After a formulary exception and a manufacturer’s discount card, her cost dropped to £120. That’s the difference between managing her condition and going without.

How Formulary Tiers Affect Real People

The system works fine for simple, common conditions. If you have high blood pressure or type 2 diabetes, you’ll likely find several affordable options in Tier 1 or 2. But it falls apart for complex, rare, or chronic diseases.Studies show that each additional tier increases the chance you’ll skip doses by 5.7%. For low-income patients, that number is even higher. A 2022 survey found 41% of people delayed or skipped treatment because of high Tier 4 or 5 costs. That’s not just a financial problem - it’s a health crisis.

Insurers say tiers save money overall. And they do - Medicare Part D saved billions by pushing patients toward generics. But those savings aren’t always passed on to you. The average copay for a Tier 1 generic is $1.27. For a Tier 3 brand-name drug, it’s $58.72. That’s a 4,500% difference. And if you’re on a specialty drug, your coinsurance could be higher than your rent.

What’s Changing in 2025?

The Inflation Reduction Act of 2022 started changing things. Now, Medicare beneficiaries pay no more than $35 a month for insulin - no matter the tier. That’s a big win. Starting in 2024, there’s also a cap on out-of-pocket spending for Part D drugs: $2,000 a year. That means even if your drug is Tier 5, you won’t pay more than that.Some PBMs are testing new models. CVS Caremark now has diabetes-specific formularies that group drugs by effectiveness, not just brand vs. generic. Analysts predict that by 2025, nearly half of commercial plans will use “value-based” tiers - where drugs are ranked by how well they work, not just how cheap they are.

But the core system won’t disappear. Tiers are too profitable for insurers and PBMs. What’s changing is the pressure to make them fairer. More states are creating drug affordability boards. More patients are demanding transparency. And more doctors are pushing back when a patient can’t afford their meds.

Final Takeaway: Know Your Formulary Before You Need It

You don’t need to be a pharmacist to understand your formulary. But you do need to check it - every year, before open enrollment. Don’t wait until you’re standing at the pharmacy counter with a $150 bill. Look up your top three meds. Write down their tiers. Ask your doctor: “Is there a cheaper option that works just as well?”Insurance formulary tiers aren’t designed to confuse you - but they’re written to protect profits. If you don’t understand them, you’re paying more than you should. Take 20 minutes now. Save yourself hundreds - or thousands - later.

What is the difference between Tier 1 and Tier 2 drugs?

Tier 1 drugs are mostly generics with the lowest copay - usually $0 to $15. Tier 2 drugs are preferred brand-name medications that your insurer negotiated a discount on. Copays are higher, typically $20 to $40. The key difference is cost: Tier 1 saves you money, Tier 2 is still affordable but more expensive.

Why is my medication suddenly in a higher tier?

Your plan’s Pharmacy Benefit Manager (PBM) may have renegotiated deals with drugmakers. If a manufacturer stops offering rebates, the insurer moves the drug to a higher tier to control costs. Changes can happen quarterly, and you might not get advance notice. Always check your formulary each year.

Can I get a non-formulary drug covered?

Yes, through a formulary exception. Your doctor must submit paperwork showing medical necessity - like failed trials of other drugs or allergies. Approval can take 7 to 10 days. Many exceptions are approved if you have strong clinical evidence. Don’t assume it’s impossible.

Are generic drugs always in Tier 1?

Almost always, but not always. Some generic drugs may be placed in Tier 2 if they’re newer, have limited competition, or if the insurer has a special deal with the manufacturer. Always verify your specific drug’s tier - don’t assume.

What should I do if I can’t afford my Tier 3 or Tier 4 drug?

First, ask your doctor if there’s a cheaper alternative. Then, request a formulary exception. Also check for patient assistance programs from the drugmaker - many offer free or discounted meds to those who qualify. Websites like GoodRx and RxSaver can also help reduce cash prices.

Does Medicare have different tiers than private insurance?

Medicare Part D plans typically use four tiers: Tier 1 (preferred generics), Tier 2 (preferred brands), Tier 3 (non-preferred brands), and a specialty tier (for high-cost drugs). Private insurers often have five tiers, with Tier 4 and 5 for specialty drugs. Medicare also has a $2,000 out-of-pocket cap in 2025, which private plans usually don’t.

How often do formularies change?

Formularies can change up to four times a year - once per quarter. Insurers must notify you if a drug you’re taking is being moved to a higher tier or removed. But notifications aren’t always clear or timely. Always review your formulary before each open enrollment period.